Quick read this month — but if you own a dental lab, this is the one to pay attention to.

Private equity already ate the dental practice market. Now they're moving one floor down — into labs. The U.S. has 6,000+ labs, most under $5M in revenue, most founder-run. That's exactly the kind of fragmented market PE loves: buy small, stitch them together, sell the platform for 2–3x what they paid in. It's not theoretical. It's happening right now.

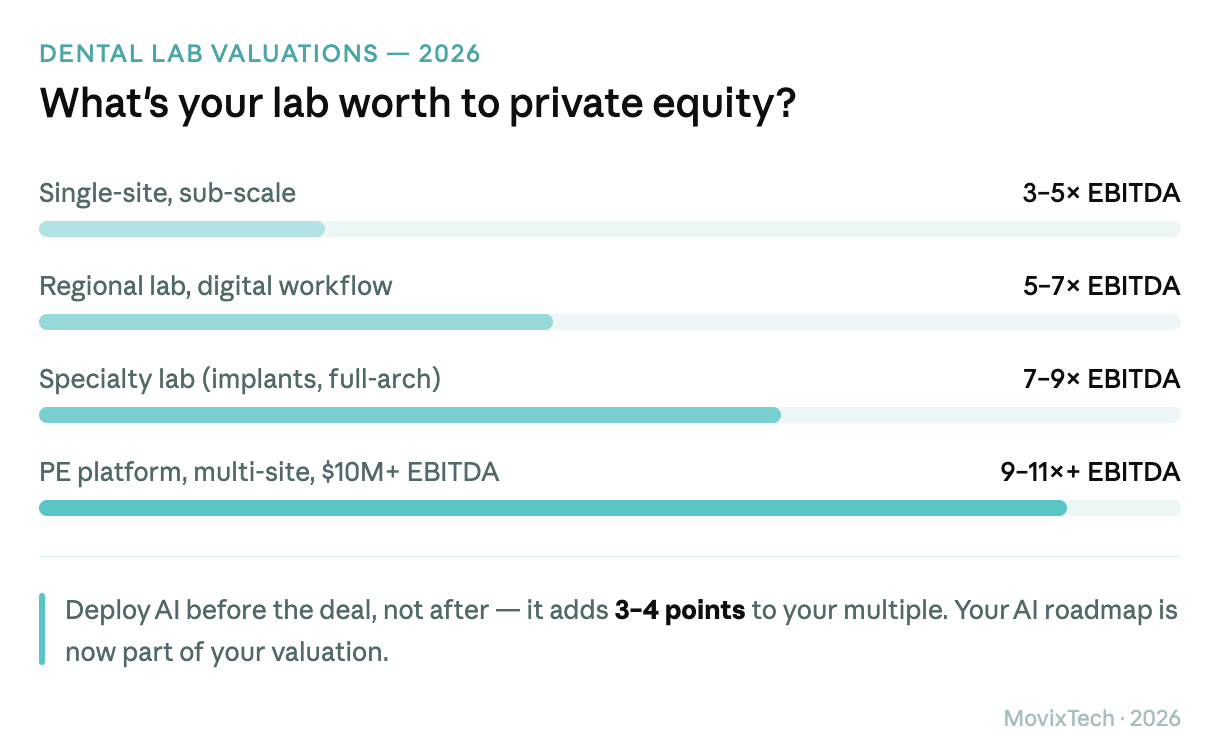

The gap between line one and line four is the entire PE thesis. Buy at 4x, plug into a platform, sell at 10x. You don't have to like it — but you should know your number.

Who's buying: NDX (Cerberus), Denbright (O2 Investment), Catalis (Caymus Equity), Zabel/Golden Ceramic(Barings), and Dandy — not PE, but the disruptor at ~$125M revenue across 6,000+ practices. If your local competitor got bought last year — you're next on someone's call list.

If you want to make more money, deploy AI before you sell — it adds 3–4 points to your EBITDA multiple. Every PE deck says "we'll deploy AI post-close." The labs that deploy before the deal capture the premium.

If you're a lab owner deciding whether to sell, scale, or sit tight — your AI roadmap is now part of your valuation conversation. Not a nice-to-have.

The next big thing isn't faster software or better equipment — it's AI dental technicians. Digital employees that actually do the work, inside the LMS and software the lab already uses. That's the category we're building at MovixTech, and it's the reason an AI-native lab in 2027 won't look anything like one in 2024.

One name to watch: Glidewell. Still private, still founder-controlled. If they move, it's the biggest event this category has ever seen. I admire Jim Glidewell — the dedication, the work ethic. That standard matters.

→ Full briefing with buyer profiles, valuation drivers, and what to watch in 2026: https://docsend.com/view/dvb7deje6xpn33uj